Most Indians spend 40 years working hard — and still retire with just enough to survive, not to live freely.

Yet a growing group of Indians started a simple ₹5,000 monthly SIP and quietly built over ₹1 crore — without picking a single stock, without reading balance sheets, without timing the market.

This is your complete guide to equity mutual funds India — what they are, how they work, which one fits your life stage, and how to use them as your personal roadmap to financial freedom.

Table of Contents

What Are Equity Mutual Funds?

Equity mutual funds are investment vehicles that pool money from thousands of investors and invest that money primarily in the stocks of publicly listed companies.

You don’t pick stocks. You don’t track markets daily. A professional fund manager does all of that on your behalf.

As per the latest SEBI regulations, an equity mutual fund must invest a minimum of 65% of its total assets in equity and equity-related instruments. This mandatory allocation is what makes these funds capable of delivering market-linked returns over the long term.

When you invest, your money gets converted into units priced at the fund’s Net Asset Value (NAV). The NAV changes every business day based on the performance of the stocks the fund holds.

Your total investment value = Number of Units × Current NAV

Simple. Transparent. SEBI-regulated.

To understand the full picture of how mutual funds work in India, read the complete guide to mutual funds in India.

Why Equity Is the Most Powerful Asset Class in India

Here is a truth most people don’t talk about: inflation in India runs at approximately 6% per year.

A fixed deposit giving 7% returns delivers a real return of just 1%. After tax, it’s even less. You are essentially running on a treadmill — moving but going nowhere.

Meanwhile, equity mutual funds India have historically delivered 12–18% CAGR over long periods — far ahead of every other asset class available to the average Indian investor.

Historical Asset Class Comparison — India

| Asset Class | Approx. Long-Term CAGR | Beats Inflation? |

|---|---|---|

| Small Cap Mutual Funds | 18–20% | ✅ Strongly |

| Mid Cap Mutual Funds | 15–18% | ✅ Strongly |

| Large Cap Mutual Funds | 12–14% | ✅ Yes |

| Gold | 10–11% | ✅ Marginally |

| Real Estate | 8–10% | ✅ Marginally |

| Fixed Deposit (FD) | 6–7% | ❌ No (post-tax) |

| Savings Account | 3–4% | ❌ No |

Data is indicative based on historical index performance. Past performance is not a guarantee of future returns.

No other asset class available to ordinary Indians comes close to equity over a 7–10 year horizon. This is not opinion. This is history.

Financial freedom is not built by saving. It is built by investing in assets that grow faster than inflation — and equity mutual funds are the most accessible way to do exactly that.

Key Costs You Must Know

Expense Ratio — The annual fee charged by the AMC for managing your money. As per latest SEBI regulations, the expense ratio for equity mutual funds is capped between 0.95% and 2.10% depending on the fund size. This is not paid separately — it is automatically deducted from the NAV daily.

Exit Load — A small charge if you redeem too early. Most equity mutual funds India charge 1% exit load if redeemed within 1 year of investment.

Growth Option vs IDCW — Always choose the Growth Option for equity mutual funds. In Growth, your returns stay in the fund and compound. In IDCW (formerly Dividend), payouts are taxed at your income slab rate — inefficient for long-term wealth creation.

Benchmark Index — Every equity mutual fund is measured against a benchmark — Nifty 50 for large cap funds, Nifty Midcap 150 for mid cap funds, and so on. The fund’s goal is to match or beat this benchmark over time. Always check how your fund performs against its benchmark — not just in absolute returns.

3 PM Cut-off Rule — If you place a buy or redemption order before 3:00 PM on a business day, you get that day’s NAV. Orders placed after 3 PM get the next business day’s NAV. This matters most for lumpsum investments during volatile market days.

To understand the difference between monthly investing and lumpsum, read SIP vs Lumpsum — which works better for you.

Types of Equity Mutual Funds in India

Equity mutual funds are not one-size-fits-all. SEBI has created clear categories so you can choose the right fund based on your risk appetite and investment goal.

Based on Market Capitalisation

Large Cap Funds — Invest minimum 80% in the top 100 companies by market capitalisation. India’s biggest and most established businesses — Reliance, TCS, HDFC Bank. Lower volatility, steady long-term growth. Suitable for conservative equity investors.

Mid Cap Funds — Invest minimum 65% in companies ranked 101 to 250 by market cap. These are companies in their prime growth phase. Higher potential returns, higher short-term risk.

Small Cap Funds — Invest minimum 65% in companies ranked 251 and beyond. Emerging businesses across niche sectors. Historically, small cap funds have delivered the highest long-term returns among all equity mutual fund categories. The reason is straightforward — a small company grows into a mid cap, then into a large cap. If you own it from the beginning through a small cap mutual fund, you participate in that entire wealth creation journey. But this requires patience — minimum 7 to 10 years.

Large & Mid Cap Funds — Minimum 35% each in large cap and mid cap. A balanced approach that captures stability and growth together.

Multi Cap Funds — Minimum 25% each across large, mid, and small cap stocks. Broad diversification across all market segments in one fund.

Flexi Cap Funds — No fixed allocation across market caps. The fund manager decides where to invest based on market conditions. Suitable when you trust the fund manager’s judgement completely.

Based on Investment Style

Active Funds — The fund manager actively selects stocks with the goal of beating the benchmark index. Higher expense ratio but potential for higher returns.

Passive Funds / Index Funds — Simply mirror an index like Nifty 50 or Sensex. No active stock selection. Lower cost. Growing rapidly among equity mutual funds India investors.

ELSS — Equity Linked Savings Scheme — A tax-saving equity mutual fund under Section 80C of the Income Tax Act. Minimum 80% invested in equity. Mandatory 3-year lock-in period — the shortest among all Section 80C instruments. ELSS delivers both wealth creation and tax savings — a dual benefit that no FD or PPF can match.

Which Equity Fund Is Right for You? (Life Stage Guide)

This is the section most financial websites skip — and it is the most important one.

The right equity mutual fund depends not just on your risk appetite, but on your life stage, your goal, and how many years you are giving your money to grow.

Use the “100 minus your age” rule as a starting point: subtract your age from 100, and that percentage is how much of your portfolio can be in equity.

- Age 25 → 75% in equity

- Age 40 → 60% in equity

- Age 60 → 40% in equity

Life Stage Equity Fund Selector

| Life Stage | Age | Investment Horizon | Recommended Fund | Why |

|---|---|---|---|---|

| Early Career | 20–35 yrs | 10+ years | Small Cap + Mid Cap | Maximum growth, time to absorb volatility |

| Growth Phase | 35–50 yrs | 7–10 years | Flexi Cap + Multi Cap | Balanced risk-return, diversified |

| Pre-Retirement | 50–60 yrs | 5–7 years | Large Cap + Index Funds | Lower volatility, stable compounding |

| Retired | 60+ yrs | 3–5 years | Large Cap / ETF | Capital protection with partial equity growth |

The logic behind Small Cap for young investors is simple. A small company today grows into a mid cap in 5 years and a large cap in 10 years. If you are invested through a small cap fund from the beginning, you participate in that full journey. That journey creates life-changing wealth.

But small cap funds demand time and emotional discipline. Expect sharp dips. Stay invested. That is the only rule.

Equity mutual funds India are a long-term tool. Use them for long-term goals.

The Real Numbers — SIP and Financial Freedom

Stop guessing. Look at the actual math.

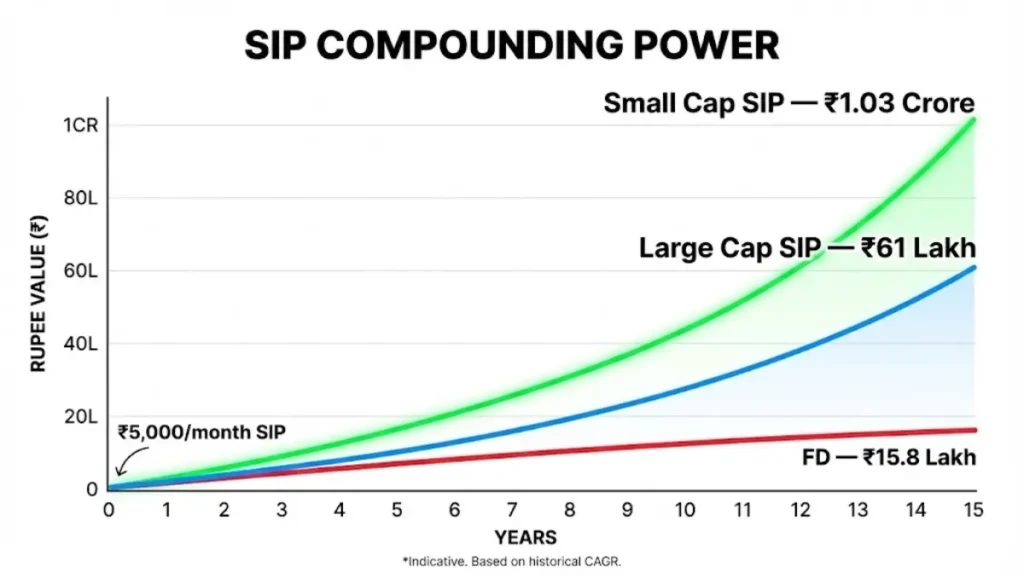

Assume a monthly SIP of ₹5,000 — less than a Netflix subscription and a dinner out.

SIP Growth Comparison — ₹5,000/Month

| Investment Option | Monthly SIP | Duration | Expected CAGR | Final Value |

|---|---|---|---|---|

| Small Cap Fund | ₹5,000 | 15 years | 18% | ~₹1.03 Crore |

| Large Cap Fund | ₹5,000 | 15 years | 13% | ~₹61 Lakh |

| Fixed Deposit | ₹5,000 | 15 years | 7% | ~₹15.8 Lakh |

| Total Invested | — | — | — | ₹9 Lakh |

Returns are based on historical CAGR averages and are for illustration only. Actual returns may vary. Mutual fund investments are subject to market risks.

You invested ₹9 lakh. The small cap SIP turned it into ₹1.03 crore. That is compounding — the most powerful force in personal finance. Not magic. Just time and discipline.

This is why India now sees over ₹31,000 crore flowing into SIP accounts every single month. Over 10 crore Indians are investing through SIP consistently. They are not doing anything extraordinary. They are simply staying the course.

The concept that makes SIP even more powerful is Rupee Cost Averaging — when markets fall, your fixed SIP amount buys more units. When markets rise, your existing units gain value. Over time, your average cost stays low and your returns compound upward.

If you are new to SIP, start with how SIP works and why it is India’s most powerful wealth-building tool.

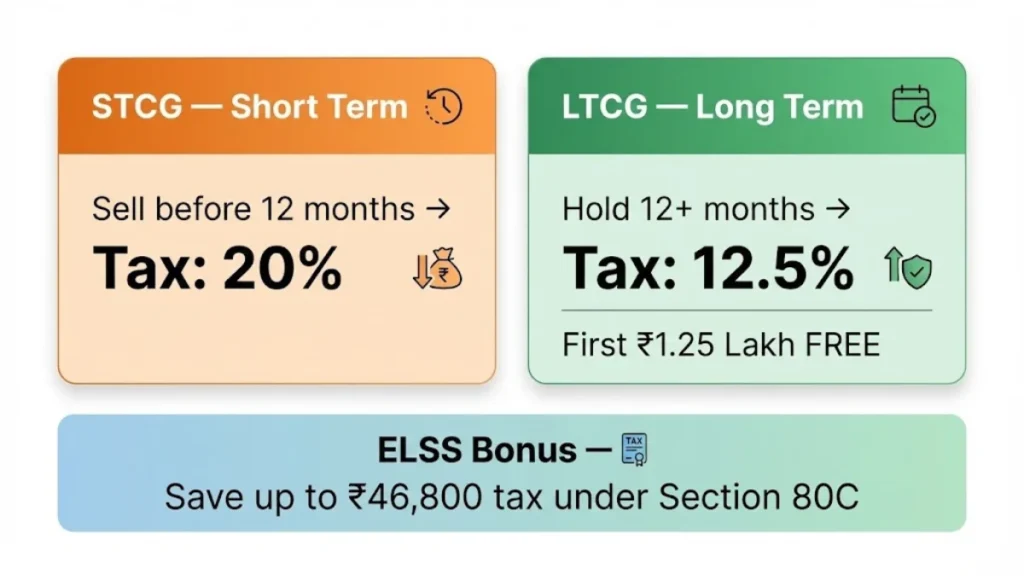

Tax on Equity Mutual Funds — What You Actually Pay

Equity mutual fund taxation in India is clear. Know this table once, and you will never be confused again.

Equity Mutual Fund Tax Rules (India)

| Tax Type | Holding Period | Tax Rate | Notes |

|---|---|---|---|

| STCG (Short-Term Capital Gain) | Less than 12 months | 20% | Applies if you sell before 1 year |

| LTCG (Long-Term Capital Gain) | More than 12 months | 12.5% | First ₹1.25 lakh per year is tax-free |

| ELSS LTCG | After 3-year lock-in | 12.5% | Same LTCG rules apply post lock-in |

| Dividend / IDCW | Any time | As per income tax slab | Added to your total taxable income |

| STT (Securities Transaction Tax) | Every buy/sell | 0.1% | Auto-charged on every transaction |

Key insight you must remember: Hold your equity mutual fund for more than 12 months, and your tax rate drops from 20% (STCG) to 12.5% (LTCG). And the first ₹1.25 lakh of LTCG every year is completely tax-free.

Long-term investing is not just smart — it is tax-efficient.

ELSS goes one step further — you get Section 80C deduction up to ₹1.5 lakh while your money stays invested in equity. It is the only equity mutual fund that gives you a tax break on the way in and LTCG benefits on the way out.

For a complete breakdown of how all mutual fund categories are taxed, read the complete guide to tax on mutual funds in India.

Direct Plan vs Regular Plan — One Decision That Costs Lakhs

Every equity mutual fund in India is available in two versions: Direct Plan and Regular Plan.

Most first-time investors don’t know the difference. This single decision can cost — or save — lakhs over a 15-year investment journey.

| Direct Plan | Regular Plan | |

|---|---|---|

| Expense Ratio | Lower (0.5–1%) | Higher (1–2%) |

| Returns | Higher | Lower |

| Intermediary | None | Distributor / Agent |

| Best For | Self-directed investors | Those who need guidance |

The 1% difference looks small. It is not.

On a ₹50 lakh portfolio over 15 years, a 1% higher expense ratio compounds into a ₹15–20 lakh difference in your final corpus. That is a real, tangible loss — simply because of the plan you chose.

If you are confident in your fund selection and investment strategy, invest through Direct Plans via platforms like MF Central, Groww, or directly through the AMC website. If you need help with goal-based planning, work with a SEBI-registered advisor or an AMFI-registered mutual fund distributor.

Benefits of Investing in Equity Mutual Funds India

- Professional Management — Expert fund managers handle research, analysis, and stock selection on your behalf

- Diversification — One fund holds 30–80 stocks across sectors — one bad stock cannot derail your portfolio

- Liquidity — Redeem your investment on any business day at the current NAV

- Affordability — Start a SIP with as little as ₹500 per month

- SEBI Regulated — Every AMC, every fund, every transaction is under strict regulatory oversight

- Power of Compounding — Returns earn returns — the longer you stay invested, the more powerful this becomes

- Tax Efficiency — LTCG exemption of ₹1.25 lakh + ELSS for Section 80C deduction

Risks You Must Know Before Investing

Equity mutual funds India carry real risks. Any advisor who doesn’t tell you this clearly is not doing their job.

Market Volatility Risk — Stock markets fall. In any given year, your equity mutual fund can show negative returns. This is normal. It is temporary. It is not a reason to panic or stop your SIP.

Real Market Cycle Proof — When COVID hit in early 2020, Indian markets crashed nearly 38% in weeks. Panic sellers locked in permanent losses. But investors who stayed invested — or increased their SIP — saw the Nifty 50 recover fully within months and go on to deliver extraordinary returns over the next 2 years. Every major market crash in India’s history has followed the same pattern: sharp fall, recovery, new highs. Time in the market always beats timing the market.

Fund Manager Risk — In actively managed funds, performance depends heavily on the fund manager’s decisions. A change in fund manager can affect future returns.

Category Risk — Small cap funds and sectoral funds experience sharper swings. A 30–40% fall in a difficult market year is entirely possible.

Concentration Risk — Focused funds and sectoral / thematic funds are highly concentrated. If that sector underperforms, your returns suffer disproportionately.

The solution to all of these risks is the same: invest with a long time horizon, stay consistent through market cycles, and never invest money you will need within the next 3 years.

5 Common Mistakes Beginners Make — Avoid These

How to Evaluate a Fund Before Investing

Don’t just pick the fund with the highest 1-year return. That is the most common and most costly mistake.

📊 Check these 4 things before investing in any equity mutual fund:

- ✔ Consistency over 5–7 years — Does the fund beat its benchmark index across full market cycles, not just bull runs?

- ✔ Fund Manager tenure — Has the same manager been running the fund for at least 3–5 years? A new manager means the track record may not apply going forward.

- ✔ Expense Ratio — Lower is better, especially for long holding periods. Compare within the same fund category.

- ✔ Portfolio turnover — Very high turnover in an active fund means frequent buying and selling, which adds costs and may indicate an unstable strategy.

The best time to start was yesterday. The second best time is today.

For a full walkthrough on choosing between monthly and one-time investing, read lumpsum investment — when and how to use it strategically. And if you are just beginning your mutual fund journey, explore best mutual funds for beginners in India.

{kind=link}

What is the minimum investment in equity mutual funds India?

Most equity mutual funds allow SIP starting from ₹100–₹500 per month. Lumpsum minimum is typically ₹1,000–₹5,000. There is no upper limit. You do not need a large amount to start — consistency matters more than the size of your first investment.

Are equity mutual funds safe?

Equity mutual funds are market-linked, not guaranteed. Short-term losses are possible and normal. Over 7–10 years, equity mutual funds India have historically delivered strong positive returns. Risk reduces significantly with a longer investment horizon and proper diversification across fund categories.

What is the difference between SIP and lumpsum in equity mutual funds?

SIP means investing a fixed amount every month. Lumpsum means investing a large amount at once. For most investors, SIP is better because it removes the pressure of timing the market through Rupee Cost Averaging — you automatically buy more units when markets fall and fewer when they rise.

Can retired investors invest in equity mutual funds India?

Yes — but selectively and conservatively. Large cap funds and ETFs provide partial equity exposure with significantly lower volatility compared to mid cap or small cap funds. These are suitable for retired investors who want some long-term growth without taking on high risk.

How long should I hold a small cap fund?

Minimum 7 years. Ideally 10 years or more. Small cap funds are volatile in the short term but have been the strongest wealth creation vehicles over long horizons in India’s market history. The logic is simple — small companies grow into mid caps and then large caps. Staying invested through that journey creates significant wealth.

What is the difference between ELSS and other equity mutual funds?

ELSS — Equity Linked Savings Scheme — offers a Section 80C tax deduction up to ₹1.5 lakh per year at the time of investing. It has a mandatory 3-year lock-in period, the shortest among all Section 80C instruments. After the lock-in, normal LTCG rules apply. It is the only equity mutual fund category that gives you a direct tax benefit on the way in and long-term capital gains treatment on the way out.

How is STCG different from LTCG on equity mutual funds?

If you sell your equity mutual fund units within 12 months of investing, gains are classified as Short-Term Capital Gains (STCG) and taxed at 20%. If you hold for more than 12 months, gains are Long-Term Capital Gains (LTCG) taxed at 12.5% — and the first ₹1.25 lakh of LTCG every financial year is completely tax-free. Holding longer is always more tax-efficient.

What is better — Direct Plan or Regular Plan in equity mutual funds?

Direct Plans have lower expense ratios and deliver higher returns over time because no distributor commission is involved. Regular Plans include a distributor who provides investment guidance and goal-based planning. On a ₹50 lakh portfolio over 15 years, the 1% expense ratio difference can compound into ₹15–20 lakh. If you are a confident self-directed investor, choose Direct. If you need structured advice, work with a qualified AMFI-registered mutual fund distributor.

Conclusion

Equity mutual funds India are not complicated. They are not reserved for the wealthy. And they are not as risky as most people think — when used correctly, with the right time horizon.

They are the most practical, accessible, and historically proven path for an ordinary Indian to build extraordinary wealth.

The Indian stock market has survived wars, recessions, global crises, and political uncertainty — and it has always recovered. Always grown. The investors who stayed invested through every storm are the ones who retired free.

You don’t need to be a financial expert. You don’t need to pick stocks. You don’t need a large lump sum to start.

You need a clear goal, a consistent SIP, and the discipline to stay invested when markets test your patience.

Start today. Stay invested. Let compounding do the work.

Your financial freedom is not a dream. It is a decision.

References & Official Sources

All data, regulations, and tax rules mentioned in this article are sourced from official Indian government and regulatory authorities.

-

1

Official source for mutual fund industry data including monthly SIP inflow figures, total AUM, number of SIP accounts, and investor education resources for equity mutual funds India.

-

2

Official source for capital gains tax rules applicable to equity mutual funds in India — including STCG at 20%, LTCG at 12.5% with ₹1.25 lakh exemption, Section 80C deduction for ELSS, and Securities Transaction Tax (STT) provisions.

-

3

Official regulatory authority governing all equity mutual funds in India. Source for fund categorization rules, minimum equity allocation requirements, expense ratio caps, exit load limits, and all scheme-related circulars applicable to AMCs and mutual fund investors.