Most people investing in mutual funds in India have never once asked themselves — why am I investing this money?

That one missing answer is costing them lakhs of rupees over their lifetime.

The best mutual funds for beginners in India are not about picking what’s trending. They are about matching the right fund to your goal, your income, and your time horizon — and this guide gives you exactly that framework.

- No goal = wrong fund. Define your goal before picking any mutual fund.

- Invest 10–15% of income if salaried; 20–30% if high income — never more than you can sustain.

- 7+ year horizon? Small cap mutual funds have historically delivered 20%+ CAGR.

- Emergency fund belongs in a liquid fund — not an FD.

- A beginner can be any age, any income — it is about starting, not the amount.

Table of Contents

Why Your Goal Decides Everything in Mutual Fund Investing

No Goal = Wrong Fund. Every Single Time

Think about it — if you don’t know what you are investing for, how will you know which fund to pick?

A person investing for retirement in 20 years needs a completely different fund than someone saving for a car in 3 years.

Yet most first-time investors in India open Groww or Zerodha, search for best SIP plans in India, and pick whatever is rated 5-star. That is not investing — that is gambling with a professional-looking interface.

Your goal is the foundation. Build that first.

How Much to Invest — Income-Based Rules That Actually Work

Middle-Class and Salaried? Follow the 10-15% Rule

If your salary is limited and your household expenses are real — don’t try to invest aggressively in amount.

Invest 10% to 15% of your monthly income via SIP. Nothing more.

This keeps your lifestyle stable and your investment consistent. And as your income grows — increase your SIP. This is called a Step-Up SIP and it is one of the most underrated wealth-building tools in mutual fund investment for beginners.

If you are unsure whether to go SIP or invest a lump sum together, the SIP vs Lumpsum comparison breaks it down clearly for Indian investors.

High Income? You Have More Options — and More Responsibility

If you earn well and your monthly investment does not disturb your lifestyle even when markets fall — you can invest 20% to 30% of your income.

At this level, you can run multiple SIPs for multiple goals simultaneously — long-term equity for wealth creation, liquid funds for emergency, and low-risk mutual funds for short-term lifestyle goals.

The Only Goal-Based Framework You Need

This is what no mutual fund investment guide for beginners actually gives you — a practical map.

Here it is.

📊 TABLE 1 — Goal vs Fund Type vs Duration

📊 Goal-Based Mutual Fund Selection — India 2026

| Your Goal | Time Horizon | Best Fund Type | Risk Level |

|---|---|---|---|

| Retirement / Financial Freedom | 15–25 Years | Small Cap / Flexi Cap | High |

| Child’s Education or Marriage | 10–15 Years | Small Cap / Mid Cap | High–Medium |

| Buy a Car or Bike | 3–5 Years | Large Cap / Multi Cap | Medium |

| Foreign Travel / Short Goal | 2–3 Years | Large Cap / Balanced | Low–Medium |

| Emergency Fund / Protection | 0–1 Year | Liquid / Debt Fund | Very Low |

| Tax Saving Under 80C | 3 Year Lock-in | ELSS Fund | Medium–High |

Selecting the best mutual funds for beginners in India becomes simple once your goal is mapped to the right fund category.

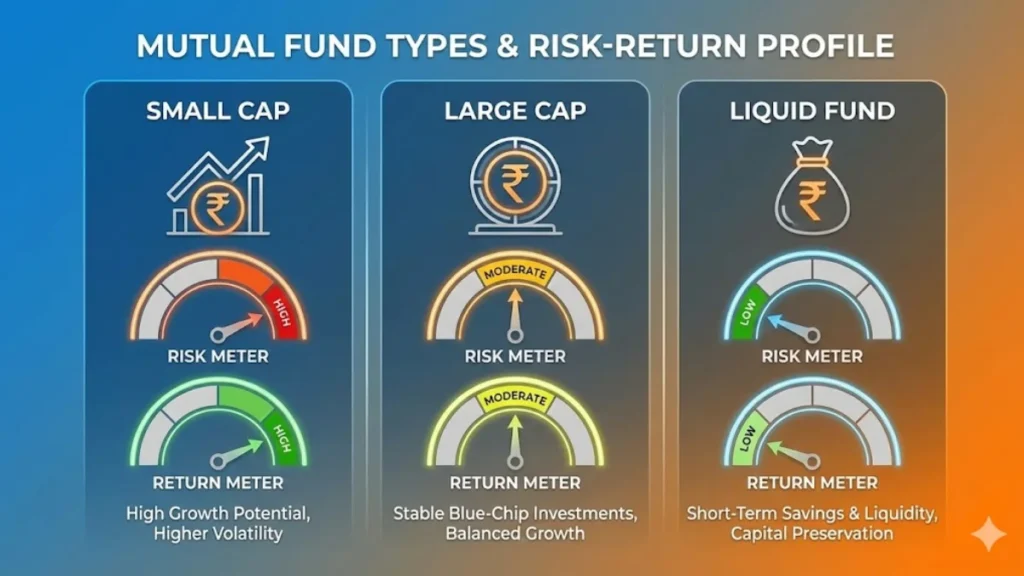

Long-Term Goals (7+ Years) → Small Cap. No Debate.

If you are investing for retirement, financial freedom, your child’s education, or their marriage — and you have 7 or more years — small cap mutual funds are your strongest option.

Yes, the volatility is highest in this category. Some quarters will test your patience.

But the data does not lie. Historically, top performing mutual funds in India in the small cap category have delivered 20%+ CAGR over 7-year+ periods. No FD, no gold, no government scheme has matched that over the same duration.

The rule is simple — longer your duration, higher the risk you can carry, and higher the wealth you will build.

Some of the consistently strong small cap funds in India include Nippon India Small Cap Fund, SBI Small Cap Fund, and Axis Small Cap Fund — all with a 7+ year track record of double-digit returns. For flexi cap exposure, Parag Parikh Flexi Cap Fund remains one of the most trusted names among long-term investors.

Before going into equity investing, understanding stock market basics will help you stay calm during market corrections instead of panic-selling.

Medium-Term Goals (3–7 Years) → Large Cap, Mid Cap, Multi Cap

Buying a car in 4 years? Planning a Europe trip every 3 years? These are medium-term goals — real, specific, and time-bound.

Large cap mutual funds work best here — stable companies, lower volatility, steady returns. Multi cap funds give you exposure across company sizes. Best mid cap funds in India sit right between growth and stability.

These are not “safe” funds — they are appropriately calibrated for your timeline.

For large cap, Mirae Asset Large Cap Fund and HDFC Top 100 Fund are well-established options. For index investing — which removes fund manager risk entirely — UTI Nifty 50 Index Fund and Nippon India Nifty 50 BeES are ideal starting points for beginners.

Emergency Fund → Liquid Fund Beats FD. Always.

Most Indians park their emergency savings in a savings account or FD. That is a costly mistake — and here is the real picture.

A liquid mutual fund gives you returns slightly better than FD, with zero exit load after 7 days, no TDS deduction, and full liquidity with T+1 withdrawal.

FD charges a penalty for premature withdrawal. It deducts TDS if interest crosses ₹50,000 (₹1,00,000 for senior citizens — Budget 2025). It locks your money when you need it most.

Debt mutual funds — especially liquid funds — are more flexible, more tax-efficient, and more accessible. For a 1-2 year emergency corpus, this is the smartest move any beginner can make.

Liquid funds like HDFC Liquid Fund, SBI Liquid Fund, and Nippon India Liquid Fund are among the most trusted options for parking emergency money in India.

“These are mentioned for reference only — always verify current performance and consult a SEBI-registered advisor before investing.”

📊 TABLE 2 — Liquid Fund vs Fixed Deposit

📊 Liquid Fund vs Fixed Deposit — Quick Comparison

| Parameter | Liquid Fund | Fixed Deposit |

|---|---|---|

| Returns | ~6.5–7.5% | ~6.5–7% |

| Liquidity | T+1 Day | Penalty on early exit |

| TDS | None | Deducted above ₹50,000 |

| Exit Load | Nil after 7 days | Premature penalty |

| Tax Treatment | Income slab — clean | Income slab + TDS hassle |

| Best For | Emergency Corpus | Fixed locked savings |

For emergency funds, liquid funds are the smarter and more flexible choice over traditional fixed deposits.

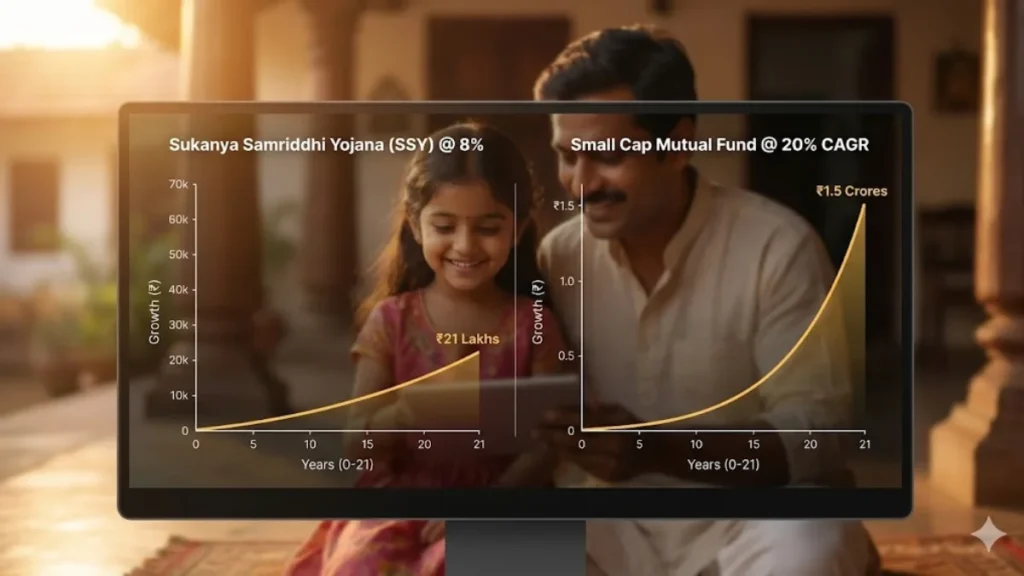

Sukanya Samriddhi vs Small Cap Mutual Fund — The Comparison Parents Never See

Millions of Indian parents invest in Sukanya Samriddhi Yojana for their daughters. It is government-backed, safe, and gives around 7–8% annual returns.

But here is the comparison you were never shown.

If your daughter is 3 years old and you invest for the next 15 years in a small cap fund — historically, that investment has delivered 18–22% CAGR over that period. The compounding difference between 8% and 20% over 15 years is not a small gap. It is the difference between a decent corpus and life-changing wealth.

This does not mean Sukanya is wrong. It means you should choose with full information — not because your neighbor did it.

For those who have a one-time amount to invest for long-term goals, the lumpsum investment guide walks you through exactly how to approach it.

“Beginner” Has No Age, No Income Bracket — Just a Starting Point

Who Exactly Is a Beginner Investor in India?

This needs to be said clearly — a beginner is not someone with less money or a lower salary.

A beginner is anyone starting their mutual fund journey for the first time.

A 45-year-old doctor investing for the first time is a beginner. A 22-year-old earning ₹18,000 starting a ₹500 SIP is a beginner. A retired government employee building a liquid emergency fund is a beginner.

The best mutual funds for beginners in India serve all of these people — just in different categories based on their goal, age, and income.

Your starting point does not define your outcome. Your consistency does.

Starting With ₹100 Is Not Small — It Is the Smartest First Step

India’s Biggest Investing Advantage in 2026

The Indian government actively promotes mutual fund investing through AMFI (Association of Mutual Funds in India).

And the best part of 2026? You can start a SIP with just ₹100 per month. That is a real option on every major platform — Groww, Zerodha Coin, Paytm Money, and direct AMC websites.

The barrier to entry has never been lower. The tools have never been better.

Use the SIP calculator to see exactly how much your ₹500, ₹1000, or ₹5000 SIP grows over 10, 15, and 20 years — the numbers will surprise you.

If you are waiting for the right time or the right amount — that day is never coming. Start today. Increase as your income grows.

For a complete understanding of how mutual funds work in India before you invest, the complete mutual fund guide covers everything from basics to advanced concepts.

Which mutual fund is best for beginners in India in 2026?

It depends on your goal. For 7+ year goals like retirement or child’s education, small cap or flexi cap funds are best. For 3–5 year goals, large cap or multi cap funds work better. For emergency funds, liquid funds are the smartest choice for beginners in India.

How much should I invest in SIP per month as a beginner?

If you are salaried or middle-class, start with 10–15% of your monthly income. If your income is high and your lifestyle is unaffected, you can invest 20–30%. Consistency matters more than the amount.

Is SIP better than lumpsum for beginners in India?

For beginners with regular monthly income, SIP is better — it removes market timing pressure and builds consistency. If you have a large one-time amount, staggered lumpsum investment works well for long-term goals.

Is mutual fund safe for beginners in India?

Equity mutual funds carry market risk and fluctuate short-term. Liquid and debt funds are far more stable. The longer your investment horizon, the lower your actual risk of loss in equity funds.

What is the minimum amount to start SIP in India?

You can start a SIP with as little as ₹100 per month on most platforms in India including Groww, Zerodha, and direct AMC websites. There is no reason to wait for a large amount.

Is liquid fund better than FD for emergency money?

Yes. Liquid funds have no exit load after 7 days, no TDS deduction, full liquidity with T+1 withdrawal, and similar or better returns compared to FD. For emergency corpus, liquid funds are the smarter choice.

Should I choose direct or regular mutual funds as a beginner?

Direct funds have lower expense ratios and deliver higher long-term returns. If you understand your investment, go direct. If you need guidance, a SEBI-registered advisor with regular funds is a reasonable option.

Conclusion: Stop Waiting. Start Right. Build Wealth.

Mutual fund investing in India in 2026 is more accessible, more transparent, and more powerful than ever before.

You now have the complete framework — goal first, income second, fund type third. You know small cap funds dominate over 7+ years. You know liquid funds beat FDs for emergency money. You know that best SIP for beginners in India is not one fund for everyone — it is the right fund for your specific goal.

No more random picking. No more following WhatsApp tips. No more waiting for the perfect time.

Pick your goal. Match your fund. Start your SIP today. Because every month you wait is compounding you are giving away.

References & Trusted Sources

This article is based on official regulatory data, government publications, and verified financial sources from India’s most trusted institutions.

-

1

Mutual Fund Industry Data — AUM, SIP flows, investor accounts, and monthly performance statistics for India.

-

2

Categorization and Rationalization of Mutual Fund Schemes — official circular defining large cap, mid cap, small cap, flexi cap, ELSS, and debt fund categories.

-

3

Monetary Policy and Interest Rate Data — used for FD rate benchmarking and comparison with liquid fund returns in India.

-

4

Sukanya Samriddhi Yojana — official scheme details, interest rate history, eligibility, and maturity rules.

-

5

Section 80C Tax Deductions — ELSS mutual funds eligibility, lock-in period, and tax-saving rules under Indian Income Tax Act.

Investment Disclaimer

This article is for educational purposes only and does not constitute financial advice. Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. Please consult a SEBI-registered financial advisor before investing.

2 thoughts on “Best Mutual Funds for Beginners in India 2026: Stop Picking Randomly — Choose by Goal, Age & Income”