Every year, millions of Indians park their savings in Fixed Deposits — trusting the bank, accepting low returns, and calling it “safe.” But safe from what — market risk, or wealth creation?

Here is what your bank will never tell you: a debt mutual fund can give you better post-tax returns than an FD, with more liquidity and no lock-in — and most investors have never even considered it.

By the end of this guide, you will know exactly what a debt mutual fund is, which type fits your goal, how it is taxed in 2026, what risks to watch, and which funds are worth your money right now.

Table of Contents

What Is a Debt Mutual Fund?

A debt mutual fund is a type of mutual fund that invests your money in fixed-income instruments — government bonds, corporate bonds, treasury bills, and money market securities. Unlike equity funds that chase stock market gains, debt funds earn returns through interest income and bond price movement.

Think of it this way: when you invest in a debt fund, the fund manager lends your pooled money to governments or companies. They pay interest, the fund earns that interest, and it reflects in your NAV (Net Asset Value) — which grows steadily over time.

Debt Fund vs Equity Fund — The Core Difference

| Parameter | Debt Mutual Fund | Equity Mutual Fund |

| Invests in | Bonds, G-Secs, T-Bills | Stocks, Shares |

| Risk Level | Low to Moderate | High |

| Return Type | Stable, Predictable | High but Volatile |

| Best For | Short to Medium Term | Long Term (5+ years) |

| Ideal Investor | Conservative / Balanced | Aggressive |

Debt funds are not a replacement for equity — they are the stability layer in your portfolio. When markets fall, your debt allocation holds the ground.

How Does a Debt Fund Generate Returns?

This is where most investors get confused — and most articles skip the explanation. Here is the full picture.

1. Interest Income (Coupon Payments)

When a debt fund holds a bond, the bond issuer pays periodic interest — called a coupon. This interest income is the most stable, consistent return component of any debt mutual fund.

2. Capital Appreciation (Bond Price Movement)

Here is where it gets interesting — bond prices and interest rates move in opposite directions. When the RBI cuts interest rates, existing bonds (with higher rates) become more valuable, and their price rises. This is called capital appreciation — and it is a big reason why 2026 is being watched closely by debt fund investors.

In 2026, with the RBI on a rate-cut cycle, long-duration debt funds like Gilt Funds and Dynamic Bond Funds stand to gain the most from rising bond prices. If you are looking to benefit from this macro trend, this is the time to understand your options.

3. Roll-Down Strategy

Some funds — especially Fixed Maturity Plans (FMPs) and Target Maturity Funds — hold bonds until maturity. This strategy reduces interest rate risk and gives investors predictable returns similar to FDs, with potential tax advantages.

7 Types of Debt Mutual Funds — Matched to Your Goal

SEBI officially categorizes 16 types of debt mutual funds. But let’s be practical. Here are the 7 types that actually matter — matched to real investor goals, not just textbook definitions.

| Type of Fund | Where It Invests | Best For | Time Horizon | Risk |

| Liquid Fund | T-Bills, CPs (up to 91 days) | Emergency corpus, salary parking | 1 day – 3 months | Very Low |

| Ultra Short Duration | Short-term debt (3–6 months) | Short-term savings goal | 3 – 6 months | Low |

| Short Duration Fund | Bonds maturing in 1–3 years | Conservative short-term goal | 1 – 3 years | Low-Moderate |

| Corporate Bond Fund | High-rated corporate bonds (80%+) | Stable returns, low credit risk | 2 – 3 years | Moderate |

| Gilt Fund | Government securities only | Rate-cut environment, safe capital | 3 – 5 years | Moderate (rate risk) |

| Dynamic Bond Fund | Flexible across durations | Active investors, rate-cycle plays | 3+ years | Moderate |

| Credit Risk Fund | Lower-rated corporate bonds | Higher return seekers | 3+ years | Moderately High |

The right debt mutual fund is not the one with the highest return — it is the one that matches your time horizon, goal, and risk tolerance. Use this table as your personal cheat sheet.

Debt Mutual Fund vs Fixed Deposit — Real Numbers, Not Assumptions

This is the comparison every Indian investor needs to see. Let’s take ₹1,00,000 invested for 3 years and compare a Bank FD at 6.5% vs a Short Duration Debt Fund at 7.5% average.

| Parameter | Bank FD (6.5%) | Debt Mutual Fund (7.5%) |

| Investment Amount | ₹1,00,000 | ₹1,00,000 |

| Gross Return (3 years) | ₹20,795 | ₹24,230 |

| Tax (30% slab — STCG/income) | ₹6,238 | ₹7,269 |

| Effective Post-Tax Return | ₹14,557 | ₹16,961 |

| Final In-Hand Value | ₹1,14,557 | ₹1,16,961 |

| Premature Exit Penalty | Yes (0.5–1%) | Exit load only (nil after 6-12m) |

| Liquidity | Restricted | Anytime (T+1 to T+3) |

Even after tax, the debt fund wins by ₹2,400+ — and that gap widens significantly for investors in lower tax brackets. For a 10% or 20% slab investor, the difference is even more in favor of the debt mutual fund. Plus, you get full liquidity — no locked-in money.

When Does FD Actually Win?

FD is better when: your tax slab is 0%, your investment horizon is under 3 months, or you need absolute capital guarantee with zero volatility. In every other scenario — compare before you commit.

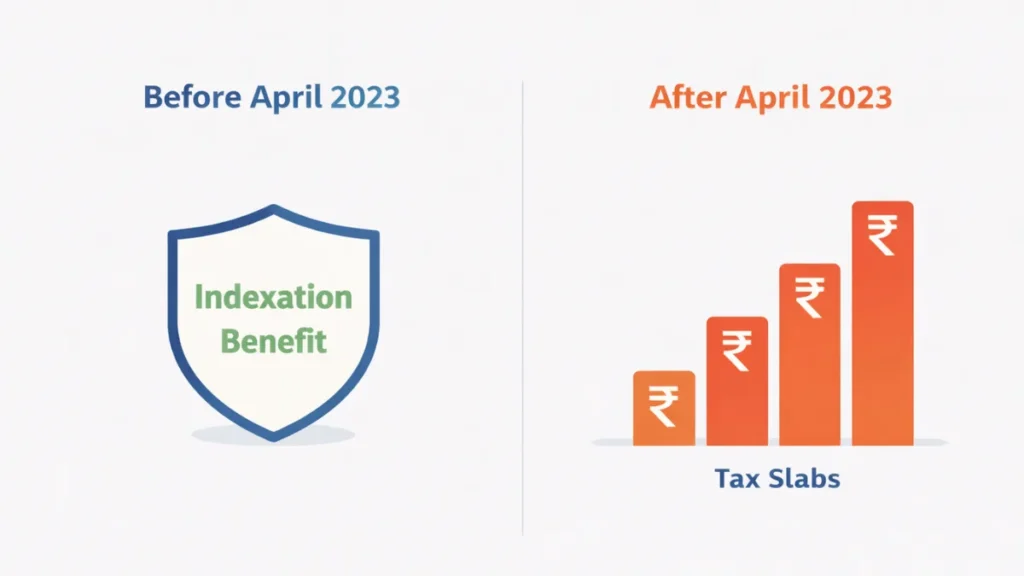

Debt Mutual Fund Taxation in 2026 — What Changed and What Didn’t

Most websites still show outdated tax rules. Here is the current, correct position as of April 2026.

The April 2023 Amendment — Before vs After

| Parameter | Before April 1, 2023 | After April 1, 2023 |

| Holding < 3 years (STCG) | Taxed at slab rate | Taxed at slab rate |

| Holding > 3 years (LTCG) | 20% with Indexation benefit | Taxed at slab rate (no indexation) |

| Indexation Benefit | Available | Removed |

| Effective tax advantage | High for long-term holders | Significantly reduced |

The indexation benefit — which helped investors reduce taxable gains by adjusting for inflation — has been removed for debt mutual funds purchased after April 1, 2023. This means both short-term and long-term gains are now taxed at your income tax slab rate.

Is Debt Fund Still Better Than FD After This Change?

Yes — for two clear reasons. First, you only pay tax when you redeem, not every year like FD interest (which is added to income annually). This deferred taxation still gives debt funds an edge. Second, returns from quality debt mutual funds are structurally higher than bank FDs. The tax change narrowed the gap — it did not reverse it.

If your tax slab is 30% and your goal is 3+ years, compare Arbitrage Funds and Equity Savings Funds — they are taxed as equity (15% STCG, 10% LTCG) and can sometimes outperform debt funds on an after-tax basis.

Risks in Debt Mutual Funds — The Ones That Actually Hurt

Debt funds are lower risk than equity — but they are not zero risk. Here are the three risks every investor must understand before putting money in any debt mutual fund.

1. Interest Rate Risk

When RBI raises interest rates, bond prices fall — and your fund NAV drops. Longer duration funds (Gilt, Dynamic Bond) are more sensitive to this. In 2022–23, many gilt funds gave negative returns precisely because rates were rising fast. In 2026, with rates stabilizing or falling, this risk is shifting in favor of long-duration funds.

2. Credit Risk

This is the risk that the company issuing a bond defaults on payment. Credit Risk Funds invest in lower-rated bonds (AA and below) for higher returns — but when defaults happen, NAV can crash sharply. The Franklin Templeton crisis of 2020 is the most important lesson here: six debt funds were shut down, ₹28,000 crore was locked, and investors waited years to recover their money. The cause? Concentrated exposure to illiquid, low-rated debt. Lesson: Never chase high yield in debt funds without checking the credit quality of the portfolio.

3. Liquidity Risk

Most debt funds allow redemption in T+1 to T+3 days. But in stress scenarios — like the 2020 Franklin crisis — even this liquidity can freeze. Stick to Liquid Funds, Ultra Short, and Banking & PSU Funds if liquidity is your top priority.

Who Should Invest in Debt Funds — and Who Should Not

Most guides only tell you who should invest. But knowing when not to invest is equally important.

✅ Invest in a Debt Mutual Fund If:

- You want to park your emergency fund (use Liquid Funds)

- You have a short to medium term goal (1–5 years) like a vacation, car, or down payment

- You want better returns than FD with more flexibility

- You want to reduce portfolio volatility — add a 20–30% debt allocation

- You are a senior citizen or retiree looking for stable income with capital preservation

- You want to take advantage of the RBI rate-cut cycle (use Gilt or Dynamic Bond Funds)

❌ Do Not Invest in Debt Funds If:

- Your investment horizon is under 1 month (use a savings account or overnight fund)

- You are expecting equity-like returns — debt is not designed for that

- Your income tax slab is 0% — an FD may be simpler and equally efficient

- You do not understand the fund’s credit quality or duration — review the factsheet first

Goal-Based Debt Fund Selector — Pick the Right Fund in 30 Seconds

Stop guessing. Use this table to match your financial goal with the right debt mutual fund category.

| Your Goal | Time Horizon | Recommended Fund Type | Risk |

| Emergency corpus | Anytime | Liquid Fund | Very Low |

| Vacation / gadget purchase | 3–6 months | Ultra Short Duration / Money Market | Low |

| Car down payment | 6–12 months | Low Duration / Short Duration | Low |

| Home down payment | 2–3 years | Short Duration / Corporate Bond | Low-Moderate |

| Child’s education (5 years) | 3–5 years | Dynamic Bond / Gilt Fund | Moderate |

| Retirement income (ongoing) | Long-term + monthly | Banking & PSU / Short Duration SWP | Low-Moderate |

| Tactical rate-cut play | 2–4 years | Gilt Fund / Long Duration | Moderate |

This is the section most debt mutual fund articles skip. Knowing which fund category to use for which goal is what separates informed investors from everyone else.

Best Debt Mutual Funds in India — 2026 (Category-Wise)

Rather than listing 50 funds, here are the top performers in each key category as of early 2026. Always check the latest factsheet before investing.

| Category | Top Fund Names | 1Y Return (Approx.) | Expense Ratio |

| Liquid Fund | Mirae Asset, Nippon India, HDFC | 7.0–7.3% | 0.10–0.20% |

| Short Duration | HDFC, Kotak, ICICI Prudential | 7.3–7.8% | 0.25–0.45% |

| Corporate Bond | Aditya Birla SL, Axis, ICICI | 7.5–8.0% | 0.30–0.50% |

| Gilt Fund | SBI, DSP, Nippon India | 8.5–9.8% | 0.30–0.50% |

| Dynamic Bond | ICICI Prudential, PGIM, Kotak | 8.0–9.5% | 0.50–0.75% |

| Credit Risk | DSP, Aditya Birla SL | 10–22%* | 0.60–1.0% |

*Credit Risk Fund returns include funds with recovered defaulted positions. These are not representative of typical returns and carry significantly higher risk. Always read the portfolio disclosure before investing in credit risk funds.

How to Invest in a Debt Mutual Fund

Follow these 6 steps to invest in the right debt mutual fund — matched to your goal, risk level, and time horizon.

Before picking any debt mutual fund, decide your goal — emergency fund, short-term saving, or medium-term growth — and your exact time horizon. This one decision determines everything else.

Match your goal to the fund type — Liquid Fund for under 3 months, Short Duration for 1–3 years, Gilt Fund for 3–5 years. Use the Goal-Based Fund Selector table in this article.

Always choose Direct Plans — they carry no distributor commission, which means a lower expense ratio and higher in-hand returns for you. Over 3 years, this difference compounds significantly.

First-time investor? Complete your KYC online via Groww, Kuvera, or MF Central. Takes under 10 minutes with just your Aadhaar and PAN — fully paperless.

Choose SIP for monthly systematic investing or Lumpsum if you have idle funds ready. For debt mutual funds, lumpsum works best when you have a clear exit timeline.

Check your fund’s credit quality, modified duration, and rolling returns every 6 months. If the fund strategy changes or credit quality drops — exit and switch without hesitation.

Pro Tip: Start with a Liquid Fund for your emergency corpus — even ₹10,000 parked there earns more than a savings account. Once that is set, move to Short Duration or Corporate Bond Funds for your next goal. One step at a time beats no step at all.

Frequently Asked Questions (FAQs)

Can I lose money in a debt mutual fund?

Yes, temporarily. If interest rates rise sharply, bond prices fall, and your NAV drops. If a bond in the portfolio defaults, the NAV can fall significantly. However, in high-quality funds (Liquid, Banking & PSU, Corporate Bond), losses are extremely rare. Choose funds with high-rated portfolios and you reduce this risk substantially.

Is a debt mutual fund better than an FD in 2026?

For most investors in the 20–30% tax bracket — yes. Debt mutual funds offer better post-tax returns, higher liquidity, and no TDS deduction. However, if you are in the 0% tax bracket or need a fully guaranteed return, an FD or small savings scheme may still be preferable.

What is the minimum investment in a debt fund?

Most debt mutual funds allow investment starting at ₹500 (SIP) and ₹1,000 (lumpsum). Some liquid funds have higher minimum amounts — always check the fund’s offer document.

Which debt fund is best for a 1-year investment?

For a 1-year horizon, Short Duration Funds or Low Duration Funds are the most suitable. They balance return potential with limited interest rate risk for a 1-year timeframe. Avoid Gilt or Long Duration funds for this period.

How are debt mutual funds taxed after April 2023?

All gains from debt mutual funds (regardless of holding period) are now taxed at your income tax slab rate. The earlier LTCG benefit with indexation for 3+ year holdings has been removed. Both short-term and long-term gains are treated as income.

Can I do a SIP in a debt mutual fund?

Yes. SIP works in debt mutual funds, though it is more useful for building a corpus for a specific goal than for volatility-averaging. It also builds a good investment discipline for conservative investors who want steady compounding without equity risk.

What happens to a debt fund when the RBI cuts rates?

When RBI cuts rates, existing bond prices rise — which increases the NAV of debt funds holding those bonds. Long-duration funds benefit the most (Gilt Funds, Dynamic Bond Funds, Long Duration Funds). This is a key reason why the 2026 rate-cut environment is being actively watched by smart debt fund investors.

Is a liquid fund safe for an emergency fund?

Yes — a Liquid Fund is the most recommended option for an emergency corpus. It offers same-day or next-day redemption (up to ₹50,000 for instant redemption), very low risk, and returns of 6.5–7.5% — significantly better than a savings account’s 2.5–4%.

Conclusion — Stop Letting Your Money Sleep in an FD

A debt mutual fund is not a complex product reserved for finance experts. It is a practical, accessible tool that gives every Indian investor — whether conservative or aggressive — a smarter alternative to the traditional FD.

You now know the types, the returns, the tax reality, the risks, and the right way to pick the right fund for the right goal. The only thing left is the decision.

Start with a Liquid Fund for your emergency corpus. Add a Short Duration or Corporate Bond Fund for your 2–3 year goals. And if you believe the RBI rate-cut cycle is real — keep a Gilt Fund in your radar.

Your money deserves better than a locked FD. Put it to work — with the right debt mutual fund.

This article is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Mutual fund investments are subject to market risks. Past performance does not guarantee future results. Please read all scheme-related documents carefully and consult a SEBI-registered financial advisor before making investment decisions.